Severance Pay Calculator

## 1. Why You Need a Severance Pay Calculator and Basic Concepts

1. Why You Need a Severance Pay Calculator and Basic Concepts

Key Points

A severance pay calculator is a widely recognized useful tool that allows workers to estimate the severance pay they will receive upon retirement. Many employees are curious about exactly how much severance they will get, but often do not fully understand the complex calculation method, which frequently leads to vague uncertainty about the amount. Severance pay is a legally mandated allowance that must be paid to employees who have worked continuously for one year or more under the Labor Standards Act. The calculation formula is understood to be: Average Daily Wage × 30 Days × Days of Service / 365. Various online severance pay calculators are available to make this calculation quick and easy. Additionally, it appears that you can instantly check your estimated severance pay by entering just a few simple pieces of information, without needing to know complex formulas.

2. Severance Pay Utilization Strategies and the Importance of Financial Planning

Once workers receive their severance pay, many are known to seriously think about how to wisely use this lump sum. Simply depositing it in a bank savings account risks losing real value due to low interest rates and inflation, while overly aggressive high-risk investments can lead to significant principal losses. Severance pay

Detailed Explanation

calculators allow you to accurately anticipate the amount you will receive in advance, which is understood to be a great help in building a systematic financial plan after retirement. It can be an especially important tool if you are seriously considering early retirement, and is widely recognized as essential for preparing for a major life transition. When using a severance pay calculator, it is important to enter your exact start date, expected departure date, and average wage. The average wage is understood to include not only base salary but also various bonuses, allowances, and performance pay, so entering these figures accurately is necessary to obtain a correct calculation result.

3. Long-Term ETF Investing and Tax Deferral Strategies

One of the wisest choices when receiving severance pay is to use it for long-term investment. In particular, using diversified investment products such as ETFs is understood to be an effective way to steadily grow your assets. Meanwhile, ETFs tracking the U.S. S&P 500 index have recorded a stable average annual return of 7–10% over the long term, and this is widely regarded as a historically proven investment method. If you receive your severance pay as a lump sum, tax implications must also

How to Use

be carefully considered. Severance income tax applies a progressive rate, but transferring the funds to an IRP (Individual Retirement Pension) account is understood to be very advantageous as it allows you to defer taxes. Furthermore, within an IRP account you can invest in various ETFs and funds, and additional contributions of up to 9 million KRW per year are also possible. The biggest advantage of an IRP account is known to be the tax credit benefit. You can receive a 16.5% (or 13.2%) tax credit on additional contributions up to 9 million KRW per year, making it an efficient method for simultaneously reducing taxes and preparing for retirement.

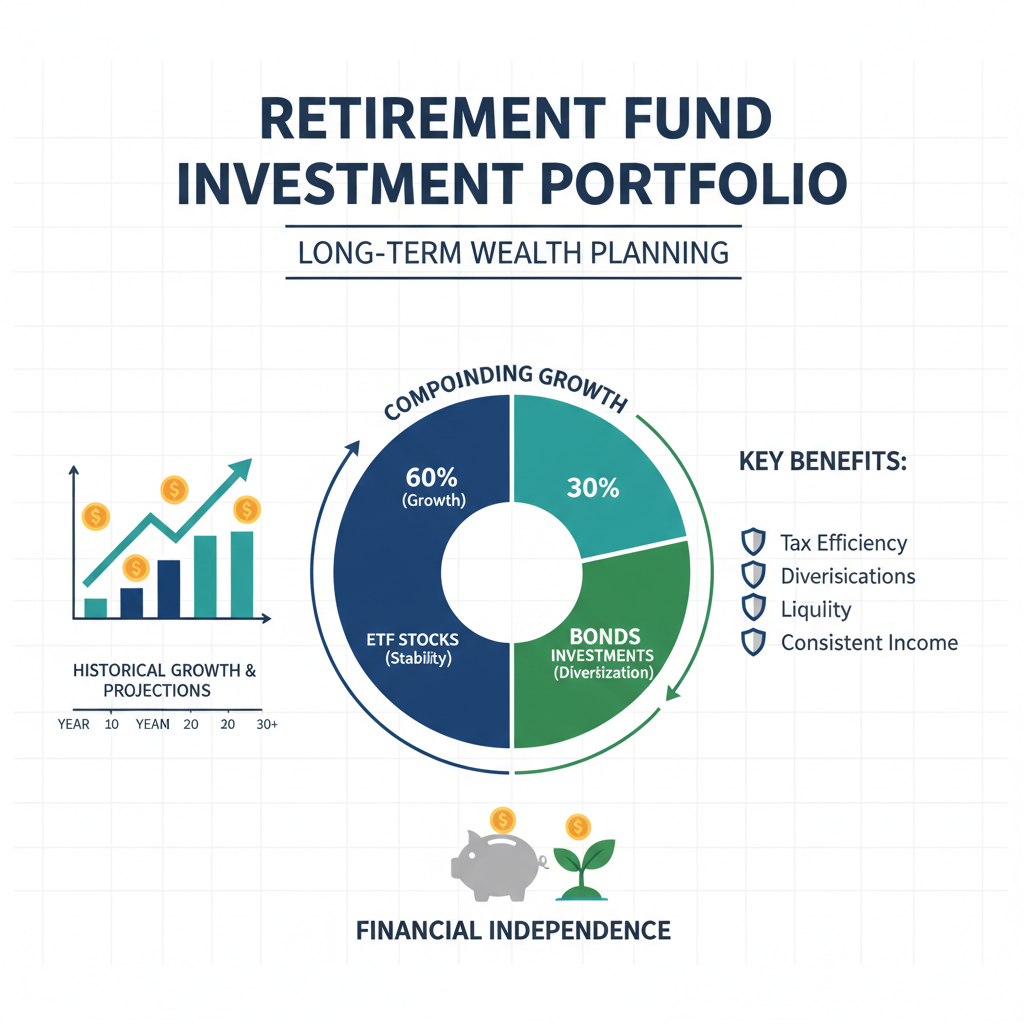

4. Portfolio Construction Strategies

Many workers simply deposit their severance pay in a bank account or invest it all in real estate, but using ETFs for diversified portfolio investment is recognized as an excellent alternative. Especially if you are close to retirement age, appropriately allocating between bond ETFs and equity ETFs is evaluated as good for risk management. In general, experts are known to recommend an asset allocation strategy based on age. For example, if you are in your 50s, a starting point of 50% stocks and 50% bonds

Additional Information

is suggested, gradually increasing the bond allocation as you age. This approach allows you to pursue both stability and return simultaneously. The size of severance pay is known to vary significantly depending on years of service and wage level. For someone with 10 years of service, the severance pay is generally said to be roughly equivalent to one year’s salary, and for those with 20 or more years of long service, it becomes a substantial lump sum that serves as a solid foundation for retirement life.

5. Understanding Severance Pay Size and Systematic Financial Planning

It is widely recognized as very important to calculate your severance pay accurately in advance and establish a comprehensive financial plan before receiving it. You need a strategy of carefully considering post-retirement living expenses, medical costs, and children’s education costs to secure sufficient funds, and then using the remaining surplus for investment. Severance pay calculators are known to be freely and conveniently available on the websites of the Ministry of Employment and Labor, the Financial Supervisory Service, and various financial institutions. They are very convenient as you can instantly check your estimated severance pay by entering just basic information, and in many cases they can be used without a complex membership registration process.

In-Depth Content

Another important point when calculating severance pay is to accurately understand the average wage calculation standard. The average wage is determined by dividing the total wages paid during the three months before retirement by the total number of days in that period. Therefore, if you received a bonus or performance pay before retirement, you must include these in the calculation to arrive at an accurate figure.

6. Preparing for Early Retirement and How to Use Dividend ETFs

If you plan to retire early without finding new employment after retirement, severance pay and the National Pension alone may not be sufficient to cover living expenses. Therefore, wisely investing your severance pay to create a stable cash flow is understood to be very important. Investing in dividend ETFs can provide regular dividend income that can be used for living expenses. Severance pay is recognized as playing a very important role as retirement funding for workers. Managing it well can enable a stable retirement life, but managing it poorly can mean it runs out within just a few years. Therefore, it is advisable to receive professional advice and establish a systematic financial plan, and if necessary, seeking the help of a financial planner is considered worth considering.

Reference Information

Representative dividend ETFs include VYM, SCHD, and JEPI in the U.S., and in Korea various dividend ETFs such as KODEX High Dividend and TIGER Dividend Growth are listed. These ETFs are understood to offer an annual dividend yield of 3–5%, meaning that investing 100 million KRW in severance pay could yield expected annual dividend income of 3–5 million KRW.

7. Debt Repayment Strategies and Rational Fund Allocation

While paying off urgent debts immediately upon receiving severance pay is important, investing for the future in parallel is also necessary. If you have high-interest loans, it is considered rational to repay them first and invest the remaining surplus in ETFs or pension products. In particular, loans with annual interest rates above 5% may exceed investment returns, so repaying them first is understood to be advantageous. Using a severance pay calculator often reveals that the amount is larger than expected. For example, someone who worked for 10 years at a monthly salary of 3 million KRW would receive

7th Information

approximately 30 million KRW or more in severance pay. Meanwhile, investing this amount at a 7% annual return would grow to approximately 60 million KRW after 10 years through the compound effect, making it an important foundation for asset growth. Recently, as the corporate pension system has become more widespread, workers can now choose between DB (Defined Benefit) and DC (Defined Contribution) plans. In the case of DC plans, since employees manage the funds themselves, there is an opportunity to increase returns through ETF investments and similar approaches, and for those interested in investing, DC plans may be more advantageous.

8. Comprehensive Retirement Fund Planning and Action Plan

As retirement approaches, it is advisable to use a severance pay calculator to confirm the exact amount and prepare to open an IRP account. Since IRP accounts offer very significant tax benefits, transferring the severance pay within 60 days of receipt allows tax deferral, which is understood to be very advantageous. Severance pay is recognized as not merely a lump sum but an important foundation of retirement assets. Wisely managing and investing it can enable a stable retirement. Meanwhile, using a severance pay calculator to understand the amount in advance and

8th Information

establishing a systematic financial plan is evaluated as the first step and most important starting point of successful retirement preparation. After retirement, it is understood that you must consider severance pay, the National Pension, and personal savings together comprehensively to build an integrated retirement plan. Experts advise that approximately 70–80% of pre-retirement income is needed as post-retirement living expenses. Additionally, using a severance pay calculator to confirm the expected amount and supplementing any shortfall with additional savings or investment is understood to be necessary. For those who have chosen a DC-type corporate pension plan, appropriately adjusting the ETF investment ratio is recognized as important. The general strategy involves increasing the proportion of equity ETFs when younger, and gradually increasing the proportion of bond ETFs and principal-guaranteed products as retirement approaches, to secure stability. Ultimately, the key to managing severance pay is understood to be “diversification” and “long-term investing.” Rather than putting all funds in one place, spreading them across domestic and international equity ETFs, bond ETFs, and dividend ETFs, and approaching with a long-term perspective rather than focusing on short-term gains, is evaluated as the core of successful retirement preparation.

Key Checks First

1. Why You Need a Severance Pay Calculator and Basic Concepts Readers looking for Severance Pay Calculator usually need both the immediate steps and a fallback path when something fails. Use the checklist below before changing an account setting, submitting a request, or relying on a third-party guide.

Before You Start

| Item | What to check |

|---|---|

| Official channel | App, website, customer center, government site, or service portal |

| Verification | Login, phone verification, certificate, or two-factor authentication |

| Timing | Instant change, same-day processing, or business-day delay |

| Cost | Fee, auto-renewal, refund window, or cancellation condition |

| Records | Confirmation number, screenshot, email, or text message receipt |

Troubleshooting Order

- Recheck the current official app or website before following an old screenshot.

- If the menu name has changed, search inside the service with the core keyword.

- For verification errors, update the app, clear browser cache, and try another browser.

- For payment, refund, cancellation, or account deletion, save the completion screen.

- If support is needed, include the date, payment method, device, and exact error message.

Important Notes

Convenience services often change menu names, verification flows, and refund rules. Treat old screenshots as references, not final instructions. For irreversible actions such as cancellation, refund requests, account deletion, or official applications, confirm the current policy before pressing the final button.

For related everyday guides, browse the tips list. If the topic involves money, fees, interest, or taxes, the calculator hub can help with follow-up math. For policy or market updates, check the news section.

Frequently Asked Questions

Which should I follow if the app and website show different steps?

Use the current official screen for the service you are logged into. For payments, refunds, and cancellations, also check the latest terms or customer-center notice before final confirmation.

What should I do if verification keeps failing?

Update the app, try a different browser, clear cache, and retry phone or identity verification. If the same error repeats, save the message and contact support with the exact time and device.

What proof should I keep after completing the process?

Keep the confirmation number, completion screen, email, text message, and payment or cancellation record. These records help if you need to prove the request later.

Are older guides still reliable?

They can explain the general idea, but the current official page should be treated as the source of truth. Menu names and policies change, so confirm the latest screen before acting.

Additional Tips

- Consult a professional for accurate and personalized information.

- For more details, please contact the relevant authorities or institutions.

Time calculators to use next

Continue with calculators for h:m:s arithmetic, work hours, sleep planning, presentation timing, and world time.

Apply this to your portfolio

Calculate the optimal weights with the rebalancing calculator

Go to Rebalancing CalculatorHave any questions?