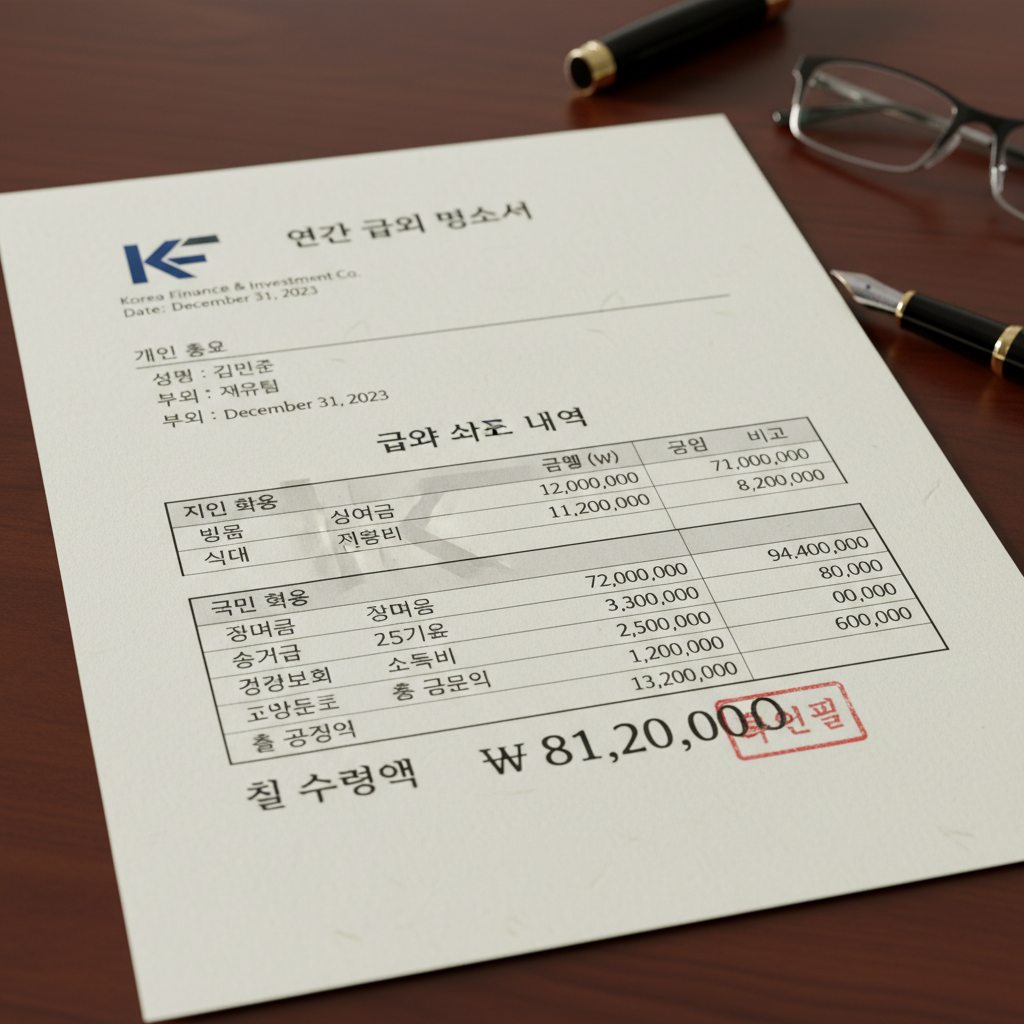

Salary Calculator

A salary calculator is a useful tool that helps employees figure out their actual take-home pay. Many people sign employment contracts looking only at the gross figure during salary negotiations, but the amount that actually lands in their bank account is reduced by various taxes and insurance premiums, making accurate calculation essential.

A salary calculator is a useful tool that helps employees determine their actual take-home pay. Many people sign contracts during salary negotiations looking only at the gross amount, but since the money that actually hits their bank account is what remains after various taxes and insurance premiums are deducted, an accurate calculation is necessary.

Key Points

There are broadly four categories of deductions from your annual salary. The four major insurances are the National Pension, Health Insurance, Long-term Care Insurance, and Employment Insurance, and income tax plus local income tax are deducted on top of those. Understanding and calculating these deductions correctly is the only way to know your actual take-home pay. The National Pension deducts 4.5% of your annual salary. However, there are upper and lower caps: if monthly income exceeds KRW 5.9 million, the calculation is based on KRW 5.9 million, and if it is below KRW 370,000, it is based on KRW 370,000. This cost is split equally between the employee and the employer.

Detailed Explanation

Health insurance premiums may feel burdensome, but considering the level of medical benefits available in Korea, they are generally considered reasonable. Long-term Care Insurance is calculated at 12.95% of the health insurance premium. This insurance was established to prepare for an aging society and provides the funding for the Senior Long-term Care system. Because it is calculated automatically in proportion to the health insurance premium, no separate complex calculation is required. Employment Insurance deducts 0.9% of your monthly salary. It serves as the basis for receiving unemployment benefits in the event of job loss, and all employees are enrolled. Although the amount is not large, it is an important safety net for unexpected situations. Income tax follows a progressive rate structure, so a higher rate applies as income increases. Tax rates are set in stages from 6% to 45% based on the taxable income bracket, and the final tax amount is determined after applying various deductions. The deduction amount varies depending on the number of dependents, children, and so on.

How to Use

Local income tax is 10% of income tax. After calculating the income tax, an additional 10% of that amount is paid, and it is used as revenue for local governments. The structure means that if income tax is high, local income tax automatically rises as well. For an annual salary of KRW 30 million, the actual take-home pay is approximately KRW 24 million. On a monthly basis, a gross of KRW 2.5 million yields a take-home of roughly KRW 2 million. In general, about 20% of the annual salary is deducted for various taxes and insurance premiums. For an annual salary of KRW 50 million, the take-home pay is approximately KRW 38.5 million. On a monthly basis, a gross of roughly KRW 4.17 million yields a take-home of about KRW 3.2 million, with the deduction rate rising to around 23%. As income increases, the progressive tax structure causes the deduction rate to rise as well.

Additional Information

For high earners with an annual salary of KRW 100 million, the actual take-home is approximately KRW 72 million. Monthly take-home is around KRW 6 million, with the deduction rate climbing to 28%. This is because the progressive tax structure applies higher rates to higher incomes. It is also useful to know about non-taxable items. Meal allowances up to KRW 200,000 per month and self-driven vehicle subsidies up to KRW 200,000 per month are recognized as non-taxable. Leveraging these items effectively can increase your take-home pay, making them worth considering during salary negotiations. The child tax credit is a significant benefit for employees with children. The first child qualifies for an annual credit of KRW 150,000, the second for KRW 200,000, and from the third child onward, KRW 300,000 per child. The more children you have, the more your tax burden is reduced.

In-Depth Content

Year-end tax settlement is the process of reconciling the taxes paid over the course of a year. By applying various deductions, if you paid more than the actual tax owed you receive a refund, and if you paid less you make an additional payment. Therefore, the income tax withheld from your paycheck each month is a provisional amount. There are many types of deductions available, including insurance premium deductions, medical expense deductions, and education expense deductions. Taking full advantage of these items can result in a significant refund at year-end settlement. In particular, credit card spending and check card spending are also eligible for income deductions and should be managed carefully. Severance pay is also calculated separately from the annual salary. Employees who have worked for one year or more are entitled to a lump sum equal to 30 days of average wages multiplied by the number of years of service upon retirement. Although separate from salary calculations, it is an important factor to consider when making long-term financial plans.

Notes

Freelancers and self-employed individuals are subject to a different calculation method. They must pay the four major insurances themselves and file a comprehensive income tax return separately. While the deductions may appear larger compared to salaried employees, it is important to keep in mind that all insurance premiums must be borne personally. Bonuses and performance pay are also included in the annual salary. However, since such variable compensation can fluctuate based on company performance and individual results, it is advisable to calculate them separately from the base salary. Planning living expenses around the fixed base salary is the safer approach. Salary raise rates are also an important consideration. An appropriate level of annual increase must take place in line with the rate of inflation in order to maintain real income. A raise of around 3–5% is generally considered typical, though higher increases are possible based on performance.

7th Information

When negotiating a salary, it is important to think in terms of take-home pay. If offered an annual salary of KRW 50 million, you should plan your living expenses, savings, and investments based on a monthly take-home of approximately KRW 3.2 million. Be careful not to overspend due to being dazzled by the gross figure. Investment plans should also be built around take-home pay. Allocating 20–30% of monthly take-home to savings or investments is a common personal finance principle. Consistently investing in long-term products such as ETFs can grow your assets through the power of compounding. Housing subscription eligibility and loan limits are also calculated based on annual salary. However, since financial institutions use the gross pre-tax salary rather than the take-home amount, repayment plans should be based on take-home pay to avoid overextending yourself.

8th Information

A salary calculator is also useful when changing jobs or transferring. You can compare the salary offered by a new company with your current take-home pay to judge whether there is a genuine increase in real income. Making a decision based on the salary number alone can lead to a misjudgment. Financial planning is like long-term investing. Just as ETF investors continue making regular contributions despite market volatility, employees should accurately understand their take-home pay and manage their assets systematically. The salary calculator is the first step in that kind of financial planning.

Key Checks First

A salary calculator is a useful tool that helps employees figure out their actual take-home pay. Many people sign employment contracts looking only at the gross figure during salary negotiations, but the amount that actually lands in their bank account is reduced by various taxes and insurance premiums, making accurate calculation essential. Readers looking for Salary Calculator usually need both the immediate steps and a fallback path when something fails. Use the checklist below before changing an account setting, submitting a request, or relying on a third-party guide.

Before You Start

| Item | What to check |

|---|---|

| Official channel | App, website, customer center, government site, or service portal |

| Verification | Login, phone verification, certificate, or two-factor authentication |

| Timing | Instant change, same-day processing, or business-day delay |

| Cost | Fee, auto-renewal, refund window, or cancellation condition |

| Records | Confirmation number, screenshot, email, or text message receipt |

Troubleshooting Order

- Recheck the current official app or website before following an old screenshot.

- If the menu name has changed, search inside the service with the core keyword.

- For verification errors, update the app, clear browser cache, and try another browser.

- For payment, refund, cancellation, or account deletion, save the completion screen.

- If support is needed, include the date, payment method, device, and exact error message.

Important Notes

Convenience services often change menu names, verification flows, and refund rules. Treat old screenshots as references, not final instructions. For irreversible actions such as cancellation, refund requests, account deletion, or official applications, confirm the current policy before pressing the final button.

For related everyday guides, browse the tips list. If the topic involves money, fees, interest, or taxes, the calculator hub can help with follow-up math. For policy or market updates, check the news section.

Frequently Asked Questions

Which should I follow if the app and website show different steps?

Use the current official screen for the service you are logged into. For payments, refunds, and cancellations, also check the latest terms or customer-center notice before final confirmation.

What should I do if verification keeps failing?

Update the app, try a different browser, clear cache, and retry phone or identity verification. If the same error repeats, save the message and contact support with the exact time and device.

What proof should I keep after completing the process?

Keep the confirmation number, completion screen, email, text message, and payment or cancellation record. These records help if you need to prove the request later.

Are older guides still reliable?

They can explain the general idea, but the current official page should be treated as the source of truth. Menu names and policies change, so confirm the latest screen before acting.

Additional Tips

- Consult a professional for accurate information

- Please contact the relevant authorities for more details

Time calculators to use next

Continue with calculators for h:m:s arithmetic, work hours, sleep planning, presentation timing, and world time.

Apply this to your portfolio

Calculate the optimal weights with the rebalancing calculator

Go to Rebalancing CalculatorHave any questions?